Zulfiqar Hasan

Topic Contents: Definition of Multinational capital budgeting, Subsidiary versus Parents perspective, Input for multinational capital budgeting, Factors to consider in multinational capital budgeting, Assessment for risk, Governance and control over international project proposal, Numerical problems

Capital budgeting & Multinational Capital Budgeting

• The process ofidentifying, analyzing and selecting investment projects whose returns (cash flows) are expected to extend beyond one year.(-James C. Van Horne)

• Capital Budgeting may be defined as the decision making process by which firms evaluate the purchase of major fixed assets including premises, machinery and equipment.

• Capital budgeting is the process of identifying, evaluating, and implementing a firm’s investment opportunities.

• Multinational capital budgeting, like traditional domestic capital budgeting, focuses on the cash inflows and outflows associated with prospective long-term (foreign) investment projects. Multinational capital budgeting has the same theoretical framework as domestic capital budgeting

Five Steps Involved In The Capital Budgeting Process

01. Proposalgeneration

Proposal generation is the origination of proposed capital projects for the firm by individuals at various levels of the organization.

02. Review and analysis

Review and analysis is the formal process of assessing the appropriateness and economic viability of the project in light of the firm's overall objectives. This is done by developing cash flows relevant to the project and evaluating them through capital budgeting techniques. Risk factors are also incorporated into the analysis phase.

03. Decision making

Decision making is the step where the proposal is compared against predetermined criteria and either accepted or rejected.

04. Implementation

Implementation of the project begins after the project has been accepted and funding is made available.

05. Follow-up

Follow-up is the post-implementation audit of expected and actual costs and revenues generated from the project to determine if the return on the proposal meets preimplementation projections.

Key Motives for Making Capital Expenditures

Expansion: The most common motive for a capital expenditure is to expand the level of operations—usually through acquisition of fixed assets. A growing firm often needs to acquire new fixed assets rapidly, as in the purchase of property and plant facilities.

Replacement: As a firm’s growth slows and it reaches maturity, most capital expenditures will be made to replace or renew obsolete or worn-out assets. Each time a machine requires a major repair, the outlay for the repair should be compared to the outlay to replace the machine and the benefits of replacement.

Renewal: Renewal, an alternative to replacement, may involve rebuilding, overhauling, or a physical facility could be renewed by rewiring and adding air conditioning. To improve efficiency, both replacement and renewal of existing machinery may be suitable solutions. These expenditures include outlays for advertising, research and development, management consulting, and new products.

Other capital expenditure proposals—such as the installation of pollution-control and safety devices mandated by the government—are difficult to evaluate because they provide intangible returns rather than clearly measurable cash flows.

Subsidiary versus Parent Perspective

Should the capital budgeting for a multi-national project be conducted from the viewpoint of the subsidiary that will administer the project, or the parent that will provide most of the financing?

The results may vary with the perspective taken because the net after-tax cash inflows to the parent can differ substantially from those to the subsidiary.

A parent’s perspective is appropriate when evaluating a project, since any project that can create a positive net present value for the parent should enhance the firm’s value.

However, one exception to this rule may occur when the foreign subsidiary is not wholly owned by the parent.

Subsidiary versus Parent Perspective

The difference in cash inflows is due to :

• Tax differentials

– What is the tax rate on remitted funds?

• Regulations that restrict remittances

• Excessive remittances

– The parent may charge its subsidiary very high administrative fees.

• Exchange rate movements

Input for Multinational Capital Budgeting

1. Initial investment

2. Consumer demand

3. Product price

4. Variable cost

5. Fixed cost

6. Project lifetime

7. Salvage (liquidation) value

8. Fund-transfer restrictions

9. Tax laws

10. Exchange rates

11. Required rate of return

Calculation of Multinational Capital Budgeting

Capital budgeting is necessary for all long-term projects that deserve consideration.

One common method of performing the analysis is to estimate the cash flows and salvage value to be received by the parent, and compute the net present value (NPV) of the project.

Multinational corporations (MNCs) evaluate international projects by using multinational capital budgeting, which compares the benefits and costs of these projects. Multinational capital budgeting involves determining the project’s net present value by estimating the present value of the project’s future cash flows and subtracting the initial outlay required for the projects. Some special circumstances of international projects that affect the future cash flow or the discount rate used to discount cash flow make multinational capital budgeting more complex

Why Multinational capital budgeting?

• Many international projects are irreversible and cannot be easily sold to other corporations at a reasonable price

• Proper use of multinational capital budgeting can identify the international projects worthy of implementation.

• It affects the profitability of a firm.

• It effect over a long time spans and inevitably affects the company’s future cost structure.

• Capital investment decision once made, are not easily reversible without much financial loss of firm

• It involves cost and the majority of the firms have scarce capital sources.

Factors to Consider in Multinational Capital Budgeting

- Exchange rate fluctuations. Different scenarios should be considered together with their probability of occurrence.

- Inflation. Although price/cost forecasting implicitly considers inflation, inflation can be quite volatile from year to year for some countries.

- Financing arrangement. Financing costs are usually captured by the discount rate. However, many foreign projects are partially financed by foreign subsidiaries.

- Blocked funds. Some countries may require that the earnings be reinvested locally for a certain period of time before they can be remitted to the parent.

- Uncertain salvage value. The salvage value typically has a significant impact on the project’s NPV, and the MNC may want to compute the break-even salvage value.

- Impact of project on prevailing cash flows. The new investment may compete with the existing business for the same customers.

- Host government incentives. These should also be considered in the analysis.

Multinational Capital Budgeting Formula

NPV = Net Present Value

i = the required rate of return on the project

n = project lifetime in terms of periods

SV = Salvage Value

CF0 = Initial investment (cash outlay)

CF1 = Cash Flow of year one

CF2 = Cash Flow of year Two

If NPV > 0, the project can be accepted.

Example 01: Multinational Capital Budgeting

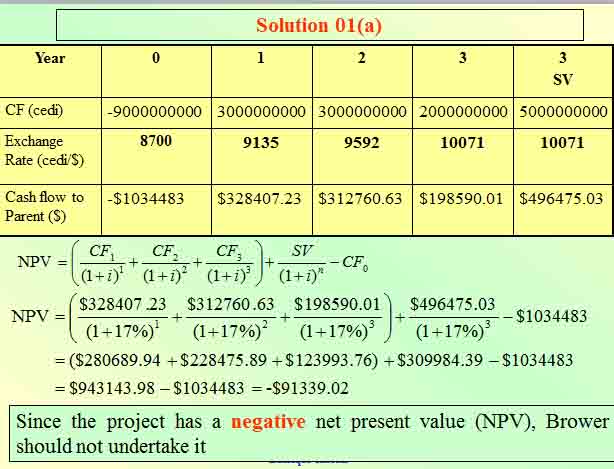

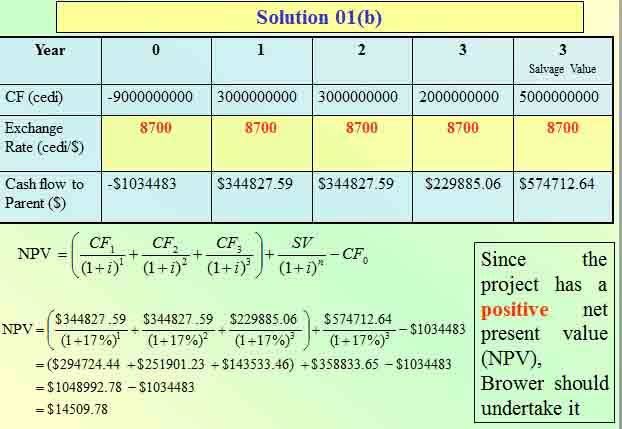

Brower, Inc. just constructed a manufacturing plant in Ghana. The construction cost 9 billion Ghanian cedi. Brower intends to leave the plant open for three years. During the three years of operation, cedi cash flows are expected to be 3 billion cedi, 3 billion cedi, and 2 billion cedi, respectively. Operating cash flows will begin one year from today and are remitted back to the parent at the end of each year. At the end of the third year, Brower expects to sell the plant for 5 billion cedi. Brower has a required rate of return of 17 percent. It currently takes 8,700 cedi to buy one U.S. dollar, and the cedi is expected to depreciate by 5 percent per year.

a) Determine the NPV for this project. Should Brower build the plant?

b) How would your answer change if the value of the cedi was expected to remain unchanged from its current value of 8,700 cedis per U.S. dollar over the course of the three years? Should Brower construct the plant then?

1Billion = 1000 million = 1000 million X 10 Lac = 100 Crore

Solution 01(a)

Solution 01(b)

Practice 01: Multinational Capital Budgeting

IBN Sina Pharmaceuticals is going to construct a medicine plant in Malyasia. IBN Sina intends to leave the plant open for Four years. Operating cash flows will begin one year from today and are remitted back to the parent at the end of each year.

|

Year |

0 |

1 |

2 |

3 |

4 |

4 SV |

|

CF |

-6.5m Ringhit |

1.5m |

2.25m |

2.75m |

3.2m |

3.2m |

The required rate of return of 13%. Current Spot Exchange Rate: BDT 18.5000/Rm. BDT is expected to depreciate by 2 percent per year.

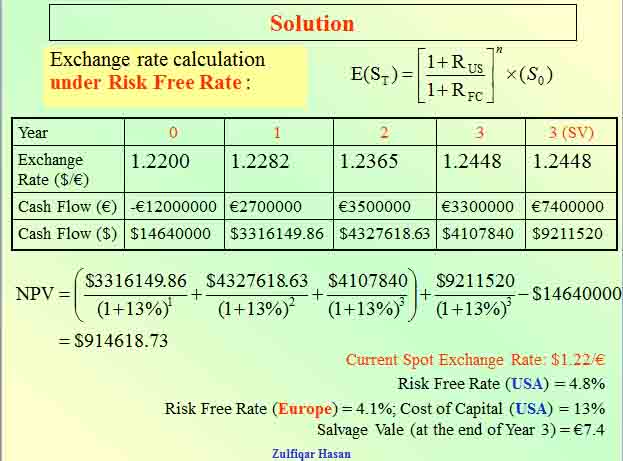

Example 02: International Capital Budgeting under Risk Free Rate

Calculate international NPV from the following information:

|

Year |

CF |

|

0 |

-€12m |

|

1 |

€2.7m |

|

2 |

€3.5m |

|

3 |

€3.3m |

Firm’s Home Country: USA

Investment Opportunity: Europe

Current Spot Exchange Rate: $1.22/€

Risk Free Rate (USA) = 4.8%

Risk Free Rate (Europe) = 4.1%

Cost of Capital (USA) = 13%

Salvage Value (at the end of Year 3) = €7.4

Solution

Exchange rate calculation under Risk Free Rate :

Practice 02: International Capital Budgeting under Risk Free Rate

Calculate international NPV from the following information:

|

Year |

CF |

|

0 |

-€10m |

|

1 |

€2.5m |

|

2 |

€3.0m |

|

3 |

€3.5m |

Firm’s Home Country: USA

Investment Opportunity: Europe

Current Spot Exchange Rate: $1.4252/€

Risk Free Rate (USA) = 4.6%

Risk Free Rate (Europe) = 4.2%

Cost of Capital (USA) = 12%

Salvage Vale (at the end of Year 3) = €6.5

Adjusting Project Assessment or Risk

• If an MNC is unsure of the cash flows of a proposed project, it needs to adjust its assessment for this risk.

• One method is to use a risk-adjusted discount rate. The greater the uncertainty, the larger the discount rate that is applied.

• Many computer software packages are also available to perform sensitivity analysis and simulation.

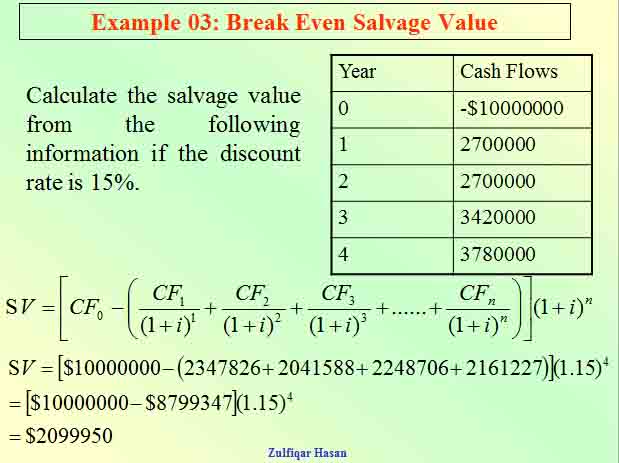

Example 03: Break Even Salvage Value

Calculate the salvage value from the following information if the discount rate is 15%.

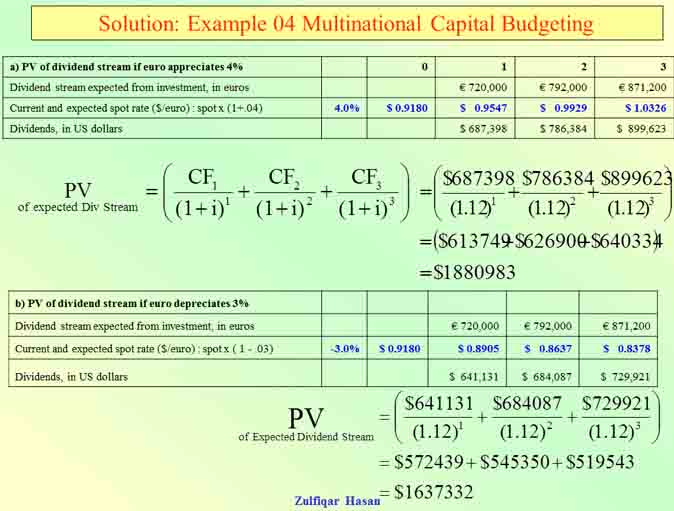

Example 04: Net present Value

Sarasota corporation , US expects to receive cash dividends from a French joint venture over the coming three years. The first dividend, to be paid December 31, 2010, is expected to be €720,000. The dividend is then expected to grow 10.0% per year over the following two years. The current exchange rate (December 30, 2009) is $0.9180/€. Sarasota’s weighted average cost of capital is 12%.

- What is the present Value of the expected euro dividend stream if the euro is expected to appreciate 4.00% per annum against the dollar?

- What is the present Value of the expected euro dividend stream if the euro is expected to depreciate 3.00% per annum against the dollar?

Solution: Example 04 Multinational Capital Budgeting

Practice 03: Net present Value

Sarasota corporation , US expects to receive cash dividends from a French joint venture over the coming three years. The first dividend, to be paid December 31, 2010, is expected to be €900,000. The dividend is then expected to grow 12.0% per year over the following two years. The current exchange rate (December 30, 2009) is $0.9070/€. Sarasota’s weighted average cost of capital is 13%.

- What is the present Value of the expected euro dividend stream if the euro is expected to appreciate 4.00% per annum against the dollar?

- What is the present Value of the expected euro dividend stream if the euro is expected to depreciate 3.00% per annum against the dollar?

Capital Budgeting: Case Analysis

The Case: Spartan, Inc., is considering the development of a subsidiary in Singapore that would manufacture and sell tennis rackets locally. Spartan’s management has asked various departments to supply relevant information for a capital budgeting analysis. In addition, some Spartan executives have met with government officials in Singapore to discuss the proposed subsidiary. The project would end in 4 years. All relevant information follows:

- Initial investment: An estimated 20 millions Singapore dollars (S$), which includes funds to support working capital, would be needed for the project. Given the existing spot rate of $0.50 per Singapore dollar, the US dollar amount of the parent’s initial investment is $10 million.

- Price and Demand: The estimated price and demand schedules during each of the next 4 years are shown here:

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

|

|

Price Per Racket |

S$350 |

S$350 |

S$360 |

S$380 |

|

Demand in Singapore |

60000 units |

60000 units |

100000 units |

100000 units |

- Costs: The variable costs (for materials, labor etc.) per unit have been estimated and consolidated as shown here:

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

|

|

Variable costs per Racket |

S$200 |

S$200 |

S$250 |

S$260 |

- The expense of leasing extra office space is S$1 million per year. Other annual overhead expenses are expected to be S$1 million per year.

- Depreciation: The Singapore government will allow Spartan’s subsidiary to depreciate the cost of the plant and equipment at a maximum rate of S$2 million per year, which is the rate the subsidiary will use.

- Taxes: The Singapore government will impose a 20% tax rate on income. In addition, it will impose a 10% withholding tax on any funds remitted by the subsidiary to the parent. The US government will allow a tax credit on taxes paid in Singapore; therefore, earnings remitted to the US parent will not be taxed by the US government.

- Remitted Funds: The Spartan subsidiary plans to send all net cash flows received back to the parent firm at the end of each year. The Singapore government promises no restrictions on the cash flows to be sent back to the parent firm but does impose a 10% withholding tax on any funds sent to the parent, as mentioned earlier.

- Salvage Value: The Singapore government will pay the parent S$12 million to assume ownership of the subsidiary at the end of 4 years. Assume that there is no capital gains tax on the sale of the subsidiary.

- Exchange Rates: The spot exchange rate of the Singapore dollar is $0.50. Spartan uses the spot rate as its best forecast of the exchange rate that will exist in future periods. Thus, the forecasted exchange rate for all future periods is $0.50.

- Required Rate of Return: Spartan, Inc requires a 15% return on this project.

Numerical Solution:

|

|

|

Year 0 |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

|

1 |

Demand (1) |

|

60000 |

60000 |

100000 |

100000 |

|

2 |

Price per unit (2) |

|

350.00 |

350.00 |

360.00 |

380.00 |

|

3 |

Total revenue (1)´(2)=(3) |

|

21000000 |

21000000 |

36000000 |

38000000 |

|

4 |

Variable cost per unit (4) |

|

200 |

200 |

250 |

260 |

|

5 |

Total variable cost (1)´(4)=(5) |

|

12000000 |

12000000 |

25000000 |

26000000 |

|

6 |

Annual lease expense (6) |

|

1000000 |

1000000 |

1000000 |

1000000 |

|

7 |

Other fixed periodic expenses (7) |

|

1000000 |

1000000 |

1000000 |

1000000 |

|

8 |

Noncash expense (depreciation) (8) |

|

2000000 |

2000000 |

2000000 |

2000000 |

|

9 |

Total expenses (5)+(6)+(7)+(8)=(9) |

|

16000000 |

16000000 |

29000000 |

30000000 |

|

10 |

Before-tax earnings of subsidiary (3)–(9)=(10) |

|

5000000 |

5000000 |

7000000 |

8000000 |

|

11 |

Host government tax rate x (10)=(11) @20% |

|

1000000 |

1000000 |

1400000 |

1600000 |

|

12 |

After-tax earnings of subsidiary (10)–(11)=(12) |

|

4000000 |

4000000 |

5600000 |

6400000 |

|

13 |

Net cash flow to subsidiary (12)+(8)=(13) |

|

6000000 |

6000000 |

7600000 |

8400000 |

|

14 |

Remittance to parent (14) |

|

6000000 |

6000000 |

7600000 |

8400000 |

|

15 |

Tax on remitted funds tax rate´(14)=(15) |

|

600000 |

600000 |

760000 |

840000 |

|

16 |

Remittance after withheld tax (14)–(15)=(16) |

|

5400000 |

5400000 |

6840000 |

7560000 |

|

17 |

Salvage value (17) |

|

|

|

|

12000000 |

|

18 |

Exchange rate (18) |

|

$0.50 |

$0.50 |

$0.50 |

$0.50 |

|

19 |

Cash flow to parent (16)´(18)+(17)´(18)=(19) |

|

$2,700,000 |

$2,700,000 |

$3,420,000 |

$9,780,000 |

|

20 |

PV of net cash flow to parent (1+i) - n´(19)=(20) |

|

$2,347,826 |

$2,041,588 |

$2,248,706 |

$5,591,747 |

|

21 |

Total PV of Cash flow |

|

$12,229,866 |

|||

|

22 |

Investment by parent (21) |

$10,000,000 |

|

|||

|

23 |

NPV= (21)-(22) |

|

$2,229,866 |

|||

Contributor: Zulfiqar Hasan is a University Teacher, working as an Associate Professor (Finance). He is pursuing PhD from IU.